I opened my drafts folder this week and had a slightly uncomfortable moment. In about two weeks I'd written that Europe starves its own scaleups, that sovereignty has no free tier, and that the money behind our flagship frontier model is a rounding error. Five posts, and the mood ranged from resigned to grumpy.

Then I went and actually added up what got switched on and signed off in Europe this year, instead of what I felt was true. The numbers were not what my last month of posts would lead you to expect.

So this is the correction post. I still think most of what I wrote holds. But I was reporting the weather from inside one specific rain cloud, and it's only fair to tell you the rest of the sky looks different.

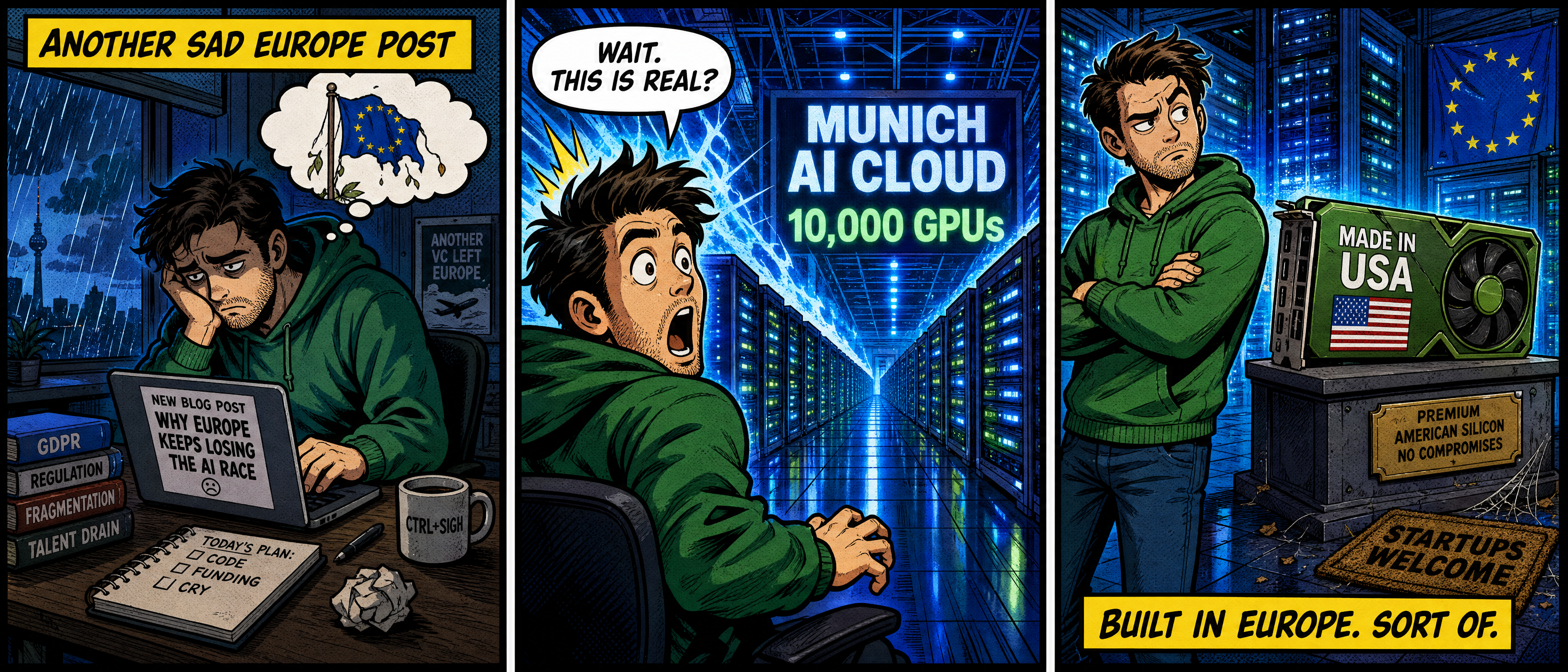

The 10,000 GPUs are real, and they're in Munich

Start with the one that made me sit up. Deutsche Telekom, the company whose customer service once made me consider a monastic life, has switched on an Industrial AI Cloud with NVIDIA in Munich. Roughly a billion euros. More than a thousand DGX B200 systems. Up to 10,000 Blackwell GPUs, half an exaflop, around 20 petabytes of storage, live as of the first quarter of this year.

That single site increases Germany's total AI compute by about 50 percent. One data center, half again as much national capacity.

And it's not a science project looking for a use. Siemens, SAP, Mercedes-Benz, BMW and a pile of robotics firms are already named as tenants, using it for the deeply un-glamorous work of simulation and digital twins and factory automation. This is the part I kept saying Europe never does. Somebody put real steel in a real building and pointed it at real industrial workloads, and it's humming right now while I type this.

It's not just Telekom

Look south and the French are, if anything, further along.

Mistral is not just raising money at a 20 billion euro valuation, it's pouring it into concrete. A 4 billion euro plan for data centers in France and Sweden, and a compute platform built on 18,000 NVIDIA Grace Blackwell chips, run on nuclear power, explicitly pitched as European infrastructure that does not sit on a US cloud. On top of that a new open-weight model, described by Arthur Mensch as "fat but sparse," which is a very French way to describe a mixture-of-experts.

The bit I underrated is the state's hand in it. This isn't a plucky startup going it alone. Bpifrance, the French public investment bank, is in the financing, Macron has been publicly telling people to use Le Chat instead of ChatGPT, and France is sitting on something like 109 billion euros of announced private AI investment. When I wrote that European companies get starved of capital and go looking for American money, Mistral is the counterexample standing in the room with its arms crossed.

The government money finally grew some zeros

This is the one that actually embarrasses me a little, because "the state won't fund it" has been a load-bearing beam in most of my sovereignty griping.

At the EU level there's InvestAI, a 200 billion euro target, with 20 billion of it earmarked for four to five AI gigafactories, each meant to hold north of 100,000 AI processors for training trillion-parameter models. Underneath that, 13 smaller AI factories have already been selected across seven countries and are ramping up now, not in some 2030 fantasy.

Germany specifically has a High-Tech Agenda worth 18 billion euros by 2029, and the federal AI budget alone hit 1.6 billion euros last year, which is more than twenty times what it was in 2017. Chancellor Merz keeps framing the combined public and private push in the 130 billion euro range.

I spent a whole post insisting the money wasn't there. The money is there. I was wrong about that, flatly, and pretending otherwise now would just be protecting my earlier mood.

Now the part I can't switch off

Here's where the correction stops being a full apology and settles into a partial one.

Almost every one of these machines is Nvidia. Blackwell in Munich, Grace Blackwell in France, Nvidia processors penciled into the gigafactories. To train on them you use CUDA, which Nvidia also owns, and Nvidia decides which chips CUDA loves. Eighteen members of the European Parliament have already written to the Commission asking, politely, how exactly a strategy to reduce dependency works when it runs entirely on one American company's silicon and one American company's software.

So call it what it is. We are building compute in Europe. We are not building the compute. We own the shed and pay the rent, Jensen owns the bricks and the blueprint, and if the export weather in Washington changes, that whole "sovereign" adjective develops a stutter.

The other asterisk is the gap between a press release and a running machine. The gigafactory bidding slipped from late 2025, to early 2026, to summer 2026, the field of interested builders narrowed from about seventy to roughly ten, and some of the funding doesn't actually land until 2028 and 2030. Critics have started using the phrase "cathedrals in the desert," which is unkind and not entirely unfair. Munich is real steel. A chunk of the rest is a ribbon and a rendering.

The floor nobody is building

And then there's the thing all of this still misses, which is the thing I keep coming back to because it's the thing I actually care about.

Every euro I just listed points upward. The Telekom cloud is for BMW and Siemens. Mistral Compute is for enterprises and governments. The gigafactories are for labs training trillion-parameter models. This is the penthouse getting wired for fibre. Wonderful. Necessary, even.

Not one line of it is the ground floor. There is still no European place where a nineteen-year-old with an idea on a Sunday can deploy something for free, on sovereign hardware, with no card and no procurement ticket. We are pouring hundreds of billions into the top of the pyramid while the bottom of it stays exactly as empty as it was. The kid who might have founded the next thing still opens a browser tab, still lands on an American free tier, still becomes an American platform's customer before anyone in Brussels has finished a sentence about sovereignty.

So my old posts aren't wrong. They just turned out to be describing a different floor of a building that is, genuinely, finally under construction.

Where that leaves my mood

I'm revising the mood, not the thesis.

The money is real, the Munich machine is real, the French are serious, and I was too quick and too glib in writing the whole continent off as all talk. That's a fair hit and I'll take it. Europe is building, right now, at a scale I'd have called optimistic in April.

I still won't believe the sovereignty word until two things are true that aren't yet. Until the silicon underneath isn't entirely on loan from one company in California. And until the on-ramp reaches the bottom, not just the boardroom.

But 10,000 GPUs came alive in Munich this year, and three months ago I'd have bet money that was still a slide in a strategy deck. I lost that bet. I'm oddly happy to have lost it, and I'm going to be watching very closely what actually gets built in those sheds, versus what just gets announced in front of them.